Plan B walkthrough: an American retiree couple, leaving the US by year-end

A reader asked us last week what Plan B actually produces. The honest answer is: a personalised report that ranks five countries, explains the visa pathway for each, and lays out a 90-day action plan. But "personalised report" doesn't show you anything. So this week we ran Plan B against a constructed profile — a realistic American retiree couple — and walked through what came back.

A note before we start: the couple below is constructed, not a real customer. We don't expose paying buyers' reports. The profile reflects the single most common type of American who buys Plan B in 2026 — recently retired, modest fixed income, decent savings, healthcare-cost anxious, six months from acting.

The profile we fed Plan B

Call them Mark and Linda — 64 and 62. Mark retired in March 2026 after 38 years as a high-school physics teacher in Ohio. Linda took early retirement two years earlier. Their kids are grown and out of state. Their mortgage is paid off. They are not wealthy by US standards, but they have what most Americans do not: about $400,000 in liquid retirement savings, plus $4,500/month in combined Social Security and a small pension.

Their immediate problem is healthcare. Mark is now on Medicare, but the supplemental plans plus drug coverage are running close to $700/month combined. Linda, two years short of 65, is paying $1,400/month on a marketplace plan with a $7,500 deductible. They are spending nearly $25,000/year before they touch a doctor.

This is the entry point. Once they start looking, the rest of the math follows: real estate they would never have bought 20 years ago, climate they want to enjoy while they can, and a political environment that, for them, has stopped feeling stable.

They signed up for Plan B and answered the form honestly:

Nationality: American

Current country: United States

Household: Couple

Monthly income: $4,500 (Social Security + pension)

Liquid savings: $400,000

Timeline: Move within 6 months

Risk tolerance: Medium-low

Motivations: Healthcare cost · Lower cost of living ·

Climate · Political stability · Tax efficiency

Visa preference: Retirement / passive-income visa

Languages: English only

Deal-breakers: Need English-language healthcare · no extreme climates

What came back is below.

The top 3 countries the system recommended

Plan B ranks five countries. We're showing the top three here in summary form. The full report goes deeper on each — and includes two more countries we're holding back for paying buyers, because the value of a $19 report is that the reasoning and the checklist are inside it, not on a public blog.

1. Portugal — 91% match

The single highest-scoring destination for this profile, and not by accident. The D7 (passive-income) visa requires €920/month per main applicant plus 50% (€460) for a spouse — so Mark and Linda need to clear about €1,380/month combined, which their $4,500/month covers roughly three times over. Healthcare is two-tier: public after residency, private from day one for around €100–€200/month each at their age. English is widely spoken in Lisbon, Cascais, Porto, and the Algarve.

A blunt note on tax, because the marketing copy on a lot of other sites is misleading: the favourable NHR regime ended in 2024. Its successor — the IFICI regime, sometimes called "NHR 2.0" — is targeted at researchers, innovation workers, and certain high-skilled professionals. Retirees on the D7 don't qualify. Foreign pensions for new arrivals are now taxed at Portugal's standard progressive IRS rates (roughly 14.5%–48%, with a high-income solidarity surcharge that can push effective rates higher). Double-tax treaties between the US and Portugal mitigate double taxation via the Foreign Tax Credit, but Mark and Linda should not move expecting the pre-2024 tax benefit. We model this honestly in the report — it doesn't eliminate Portugal as the top choice, but it does change the after-tax math significantly versus what the older guides suggest.

What knocks Portugal down from a higher score: the May 2026 citizenship law extension (5 years to 10 years for most nationalities, per our full analysis — though permanent residency stays at year 5, so the lifestyle math holds), the rental market in Lisbon (still cooling but not cheap), and a realistic 6–18 month visa-to-arrival timeline if Mark and Linda start now.

2. Mexico — 89% match

A close second, and the destination most retirees underestimate. The Temporary Resident Visa now requires roughly $4,300/month in passive income under Mexico's new UMA-based calculation method (effective 2026, replacing the prior minimum-wage formula). Mark and Linda clear it with margin. After four years on Temporary Resident, they're eligible to convert to Permanent Resident automatically.

Mexico doesn't require you to give up Medicare. Many American retirees keep it for serious procedures in the US and use Mexican private insurance — running roughly $300–$500/month per person at Mark and Linda's age with major insurers like AXA, MetLife, or GNP — for routine care. The IMSS public system is technically available after residency at a fixed annual contribution but is slow; private hospital infrastructure clusters in CDMX, Guadalajara, Mérida, San Miguel de Allende, and the Riviera Maya.

One thing to flag clearly because the older expat literature gets it wrong: Mexico has a worldwide tax system for residents, not a territorial one. If Mark and Linda spend 183+ days/year in Mexico — which they would under the TR visa — they become Mexican tax residents and owe Mexican income tax on their worldwide income, including US Social Security and pension. The US-Mexico tax treaty mitigates double taxation via the Foreign Tax Credit, but the framework is fundamentally different from Costa Rica's, and it's the single most-misreported point in the Mexico-for-retirees space.

What knocks it down: USD-MXN volatility (the peso strengthened sharply through 2025), a politically uneven environment by state, and the constant low hum of personal-safety planning that varies meaningfully by region.

3. Costa Rica — 85% match

The most Plan-B-classic destination on the list. The Pensionado visa needs only $1,000/month in lifetime pension or Social Security income — Mark and Linda qualify with $3,500/month to spare. The Central Valley (San José, Escazú, Heredia) clusters bilingual private hospitals with a quality reputation that pulls medical tourists from the US. The Caja public system is available after residency at a fixed percentage of declared income.

Costa Rica uses a territorial tax system — residents are taxed only on Costa Rica-source income. US Social Security and US pensions stay outside the local tax net. This is the structural tax advantage Mexico and Portugal don't offer, and for a couple living entirely on US-source retirement income, it can be worth several thousand dollars per year.

What knocks it down: cost of living has risen sharply since 2020 (now closer to Mexico than to Panama at most price points), real-estate inflation in Guanacaste and the Central Valley, and a slow but real bureaucratic backlog through 2026 on Pensionado approvals.

Plus two more we are holding back

Plan B returned five countries. The bottom two — both legitimate matches for this profile, but with specific trade-offs around income thresholds, tax angles, or healthcare access — sit in the paid report. That's the part that genuinely can't be guessed from country guides.

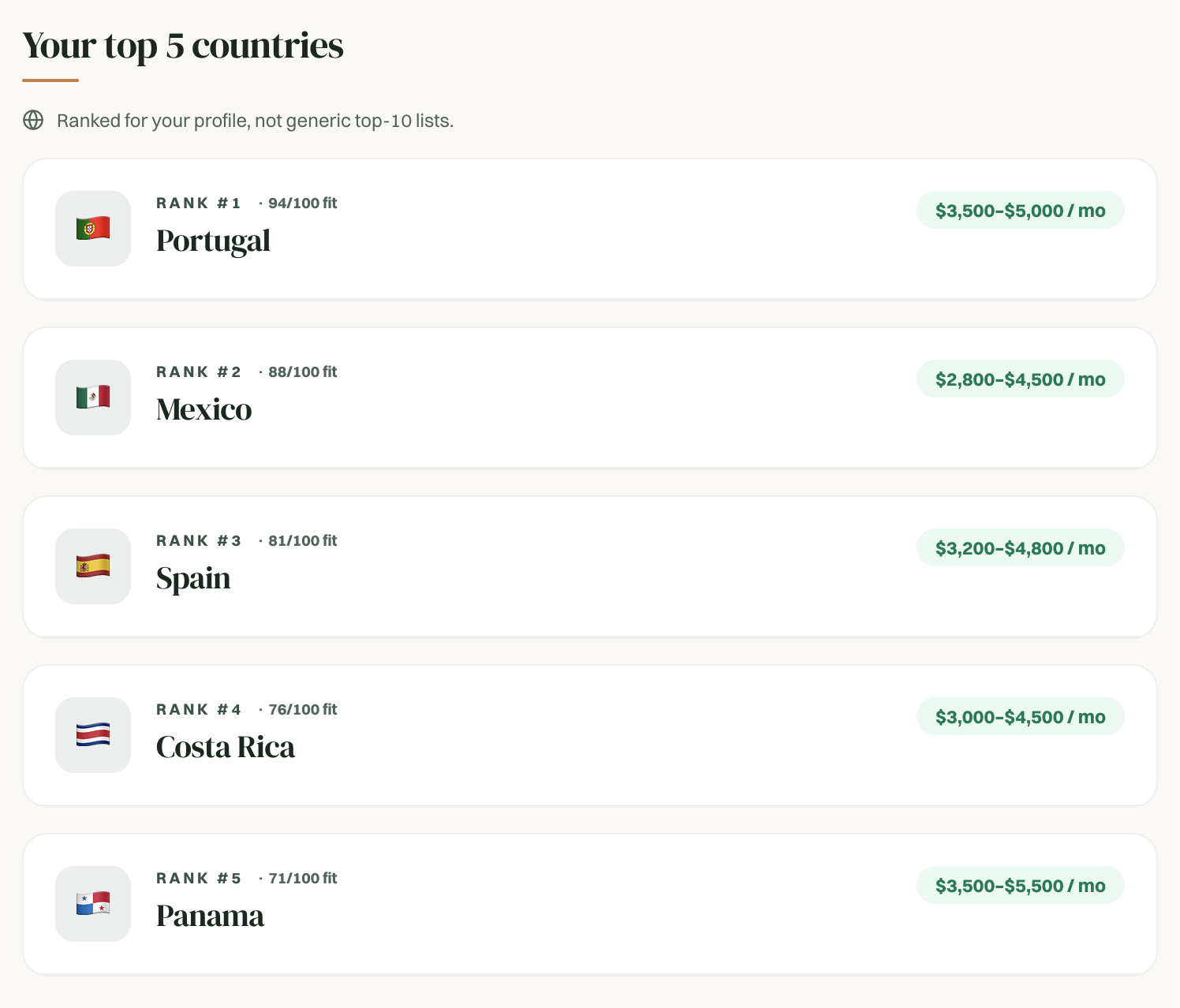

The "top 5 countries" panel from the public Plan B sample report. Note that the sample uses a different profile — an American family of 4 — so the rankings and match percentages shown here are from that profile, not Mark and Linda's. The structure of the output is the same.

What the 90-day plan looks like (summary)

Plan B doesn't just rank countries. The second half of the report is a concrete 90-day action sequence, broken into three phases. For Mark and Linda the milestone titles look like this:

Days 1–30 — Documents and visa pre-application. Birth, marriage, FBI background checks (with apostille). US bank-statement letter. Pension and Social Security award letters. Medical exams scheduled.

Days 31–60 — Healthcare, tax setup, and money pipeline. Private health insurance researched and quoted. US tax-residency exit checklist reviewed with a cross-border CPA. International bank account opened. Wise / Revolut / Mercury USD-to-local pipeline tested with a small transaction.

Days 61–90 — Visa submission, pack-out, and landing. Visa application filed with the consulate. Belongings triaged into ship / store / sell. One-way flight booked. First-month rental locked in at destination, not bought sight-unseen.

The full report includes the actual line-items inside each phase — the specific documents, the specific consulate booking links, the specific cross-border accountants we recommend talking to. That detail is what separates the report from a generic "moving abroad checklist."

Why this profile is worth showing

We picked Mark and Linda because they represent the single most common kind of person buying Plan B right now: not the wealthy retiree with a foreign passport already in hand, not the tech worker with a remote job. The middle-class American retiree, anxious about healthcare and cost of living, with enough savings to act once but not enough to make multiple mistakes.

If that profile is yours — or close to yours — Plan B will produce something tighter and more personal than this walkthrough. The $19 buys two things: the two countries we held back here, and the full per-country reasoning and 90-day checklist instead of the summary above.

Research and drafting assistance: Claude (Anthropic). Editorial review, country and visa data, and final responsibility: ExpatLife Editorial Team, June 2026.

This article describes general country and visa information and does not constitute tax, legal, or immigration advice. Tax treatment of foreign pensions and Social Security varies by country and individual circumstance — consult a US-qualified cross-border CPA and a licensed immigration lawyer in your destination country before making decisions.

Your personal Plan B · $19 one-time

Don't just read — plan.

Top 5 countries ranked for you, the visa pathway for each, tax angle for your nationality, and a concrete 90-day action plan. Built in ~2 minutes from current 2026 data.

Enjoyed this article?

Subscribe for more expat tips and guides.

Which country is right for you?

Answer 6 quick questions about your budget, lifestyle, and priorities. Our AI ranks 122 countries and builds a personalised relocation plan.

Enjoyed this article? Share it with fellow expats